Readers of Jane Austen’s novels from outside England have the disadvantage of knowing less than many English readers do about the cultural and legal background that she assumed her readers would have. The following essay—written for the “Global Jane Austen” conference at the University of Southampton in July 2025—seeks to inform the global reader about some of these potentially unfamiliar legal topics.

1. Entails and real property law

Jane Austen’s original readers would have recognized the existence of an entail in every one of her novels. The references are explicit in Pride and Prejudice and Lady Susan; implicit but necessary to full understanding of the plot in Sense and Sensibility, Emma, and Persuasion; and of only tangential interest in Northanger Abbey and Mansfield Park.1

It is necessary to start with a short excursion into English land law of the time. Land was held in big estates. You did not own your house; someone owned the village and the surrounding land. Highbury is a good example. Two families own everything in and around the village. The prime consideration of landowners was to keep the estate together so that it would move down the male line from eldest son to eldest son (although the law itself was completely receptive to female heirs). The entail was a useful vehicle to achieve this intact transmission. An entail is an estate in land that automatically goes from the current holder to the (normally male) heirs of his body. The odd name derives from taillé, meaning cut down, in the sense that it is a cut-down freehold, because a freehold could descend to collateral heirs like nephews, but an entail had to descend to heirs of the body only.

Entails existed as part of a strict settlement, often a marriage settlement—a trust under which land was held by a tenant for life (tenant just meaning holder and having nothing to do with leases); then an entail to, normally, his eldest son (the tenant in tail) and the heirs of his body (and the same for the second and successive sons, in case the eldest son had no heirs of his body); in case the entail died out, the estate would pass to a remainderman (think of Mr. Collins). There was, however, one disadvantage: any tenant in tail could bar (or terminate) the entail at the age of twenty-one and make the land his own property absolutely—although barring the entail required the consent of the prior tenant for life if he were still living. Barring entails—that is, making the holder into the absolute owner—was an invention of the courts. This legal strategy was, in fact, totally contrary to an Act of Parliament of 1285, but it was necessary for entailed land to be saleable; otherwise, each tenant in tail could sell only his life interest, which would be of no interest to a purchaser. One might have thought that Parliament would have changed the 1285 law, but the members of the House of Lords were big landowners who were intent on keeping land in their families and did not want to sell it, so they never agreed to a change.

One further aspect of strict settlements should be mentioned. Despite being in trust, the tenant for life (as well as each tenant in tail) held the land in his own name and had wide powers of dealing with it. He might even be able to sell it, probably after giving notice to the trustees or with their consent—but that was not of great interest, as the money would go to the trustees to be held on the terms of the trust so that he would receive the income only. Even if Sir Walter Elliot does “condescend to sell” (P 10) the small part of the Kellynch estate that he has power to dispose of, he will not receive the proceeds, although he will receive the income from the proceeds. Similarly, while he has condescended to mortgage the estate so far as he has the power, it is most unlikely that he has the power to mortgage it for his own benefit, as opposed to benefiting the estate or providing portions for his daughters (as we shall see below).

In practice, the system worked like this: As soon as the tenant in tail turned twenty-one, his father (the current tenant for life) would lean on the son to make him bar the entail on terms that the father would consent to only if the son resettled the land on himself for life followed by entail to his eldest son, thus creating a new entail. Why would the son agree? If he didn’t, he would have to wait until the father’s death to have any income. Being just twenty-one, he desperately wanted an income, and to persuade him to bar the entail and create another entail for his eldest son, his father would agree to give up some of his income during the father’s lifetime. The process would be repeated when the grandson was twenty-one.

We can now fit this system into the novels.

This chart brings some of the family property relationships into clearer focus. In Lady Susan, although Reginald is over twenty-one, it seems that he has not barred the entail, perhaps suggesting a level of trust between father and son. Sir Reginald writes to Reginald: “‘You know your own rights, and that it is out of my power to prevent your inheriting the family Estate’” (LM 22). On the other hand, given Tom Bertram’s unreliability, Sir Thomas has surely made him bar the entail and resettle the estate on reaching age twenty-one. In Pride and Prejudice, Lady Catherine draws a distinction between the disposition of Longbourn and that of Rosings: “‘I see no occasion for entailing estates from the female line.—It was not thought necessary in Sir Lewis de Bourgh’s family’” (185). The Rosings arrangement must be a tail general, under which heirs of the body of either sex can inherit. Finally, William Walter Elliot is the great-grandson of the second baronet—and, I assume, the descendant of a younger son—whereas Sir Walter (the fourth baronet?) is the descendant of the elder son; this relationship makes him Sir Walter’s “Heir presumptive,” as he is correctly described in Sir Walter’s manuscript addition to the Baronetage (4).

A recurrent theme in Austen’s novels relates to the current absence of a tenant in tail (while the possibility of a future holder still exists), or the presence of an heir presumptive who will be ousted by someone born subsequently with a better claim (hence the designation “None currently living” in the table). Like Mr. Collins, we can in practice discount the possibility that if Mr. Bennet survives his wife, he might marry again and have a son. But the possibility is far more real for Sir Walter Elliot, a widower; hence William Elliot makes Mrs. Clay his mistress to prevent her from marrying Sir Walter. If Mrs. Clay and Sir Walter were to marry and have a son, the son would be entitled to the entail (and also the baronetcy), and William would have nothing: “it was evident how double a game he had been playing, and how determined he was to save himself from being cut out by one artful woman, at least” (273). For similar reasons (in part), when Emma thinks that Mr. Knightley might marry Jane Fairfax, she is against the marriage: “‘Mr. Knightley must not marry!—You would not have little Henry cut out from Donwell?’” (E 242). The son of Mr. Knightley (the eldest son) would have priority over little Henry, the son of John Knightley (the younger son) and Emma’s sister, who is only presumptively entitled to the entail.

Austen was not particularly interested in the means of keeping the land in the male line. She was far more interested in how females and younger sons were treated. For women and younger sons, there were no typical arrangements; each settlement was defined on its own terms. Settlements would often provide for a jointure (annuity) for a widow and portions (lump sums of a fixed amount) to children other than the eldest son, who would inherit the estate. Mr. Collins, as one would expect, uses the term correctly: “‘Your portion is unhappily so small that it will in all likelihood undo the effects of your loveliness and amiable qualifications’” (PP 122). It would not have been unusual if the Longbourn settlement had provided an entail for daughters equally if there were no sons, but it did not. The Norland settlement did not contain any jointure, and the portions for the daughters were small.

The mechanism for providing lump sum portions out of illiquid land was that the settlement would provide for separate trustees (called portions trustees) to have a rent-free lease of 100 or more years following the tenant for life and before the tenant in tail. To provide the lump sum portions, this lease could be mortgaged without affecting the title to the whole land. The interest would reduce the income of the tenant for life if mortgaged in his lifetime (which was possible even though the lease was in the future). He might mortgage the lease, for example, to give daughters their portion on marriage, subsequently reducing the income of the tenant in tail. The tenant in tail would eventually pay off the mortgage, often by selling timber. Hence the reference to the Norland estate being secured “in such a way, as to leave to [Henry Dashwood] no power of providing for those who were most dear to him, and who most needed a provision, by any charge on the estate, or by any sale of its valuable woods” (SS 4, emphasis added).2 The reason why Anne Elliot will receive “but a small part of the share of £10,000 which must be hers hereafter” (P 270) is that Sir Walter cannot stand the loss of income he would experience if the lease were mortgaged to provide portions to all the daughters. A more indirect reference is that Henry Tilney’s fortune from marriage settlements means that he has good portions under the settlements, presumably separate ones made by both parents.

Only land could be entailed, not personal property (except heirlooms, which are very narrowly defined). When Mrs. Bennet notes that “[t]he hall, the dining room, and all its furniture were examined and praised [by Mr. Collins]; and his commendation of everything would have touched Mrs. Bennet’s heart, but for the mortifying supposition of his viewing it all as his own future property” (PP 73), she is wrong about the furniture, which cannot have been entailed and is unlikely to have been in trust because of the difficulty of the trustees’ keeping track of it. Another example is that the books and bookshelves in the library at Godmersham could not be entailed with the house, but Edward Knight’s will provided that the library was left to trustees, to allow the current tenant in tail of the house to use it.

There are a few examples of the even worse situation for females when there was no settlement. In The Watsons, Mr. Turner has left his estate outright to his widow, and when she remarries, Emma Watson’s expectations come to an end. As her attorney brother says, “‘How the devil came he to make such a will? . . . He might have provided decently for his widow without leaving everything that he had to dispose of, or any part of it, at her mercy’” (LM 123). Similarly, Sanditon’s Mr. Hollis left all his property to his widow, now Lady Denham. Though she has also outlived Sir Harry Denham, he did not leave his estate to her: “‘Not a shilling do I receive from the Denham estate’” (LM 178).

2. The clergy

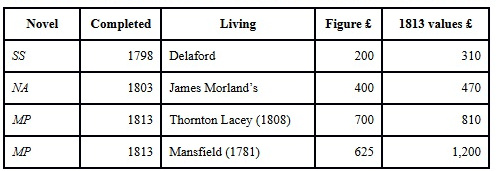

The novels are replete with references to clergymen holding a “living,” and in a few cases the value of the living is given. The rector was paid by tithes, a tenth of the agricultural produce of the parish. Originally this produce was paid in kind and stored in a tithe barn, many examples of which can still be seen—but in Austen’s period the clergyman’s income was likely to be an agreed amount paid in cash, with the amount reviewed periodically. The Delaford living, for example, “did not make more than 200l. per annum, . . . though it is certainly capable of improvement” (SS 320), meaning that there is scope for renegotiation. As a tax on the produce rather than on the profit, tithes were unpopular. Adam Smith disapproved of their economic effect, describing them as “a great discouragement both to the improvements of the landlords and to the cultivation of the farmer” (Smith V.ii.d.3). James Stanier Clarke, chaplain and librarian to the Prince Regent (to whom Emma was dedicated), suggested that Austen write a book about a clergyman which would “shew dear Madam what good would be done if Tythes were taken away entirely” (Austen, Letters ?21 December 1815). Not surprisingly, she declined; her father had depended on them, as her brother James currently did. The amount of the living thus depended on the size of the parish and the fertility of the land.

Holding more than one living was known as pluralism and required permission. Austen’s father obtained permission to hold the adjoining livings of Steventon and Deane. James Austen held three. Being an absentee rector was discouraged. Sir Thomas Bertram would be “‘deeply mortified’” if Edmund were not resident in Thornton Lacey as rector, even though it is only eight miles away from Mansfield (MP 288). The rector could appoint and pay a curate to help with the duties, or, in the case of an absentee rector, to carry out all the duties. Curates were not well paid; Mrs. Jennings thinks Edward Ferrars may have to settle for “‘a curacy of fifty pounds a year’” (SS 313) if he marries Lucy Steele. Some years later, in 1816, Henry Austen’s first clerical job was the curacy at Chawton, with an income of 52 guineas (£54.12.0).

The right to present a person to a living, whom the bishop would, subject to some exceptions, automatically appoint as rector, was called an advowson. Advowsons were a species of real property and devolved in the same way as physical land. A landed estate would normally have one or more advowsons that went with it. The holder would thus be able to present a younger son, who would not inherit land, as rector and give him a living. Sir Thomas Bertram holds the advowsons of Mansfield and Thornton Lacey, and he initially uses the latter to appoint Edmund as rector.

Advowsons, like any other land, could be sold or leased, and the right to make the next presentation could also be sold separately, but the law of simony restricted this right by making the transaction void if the living was vacant. Unable to believe that Colonel Brandon has failed to make money by selling the right to the next presentation before it becomes vacant, John Dashwood wrongly assumes that it has been sold, that Edward Ferrars is merely to hold the living until the purchaser’s nominee is old enough to be ordained, and that he has promised to resign when that occurs. Learning the truth, John Dashwood regretfully acknowledges, “‘Now indeed it would be too late to sell it’” (SS 334). In Persuasion, Charles Hayter has “been applied to by a friend to hold a living for a youth who could not possibly claim it under many years” (P 235)—an arrangement that enables him to marry. Henry Austen held the living at Chawton until Edward’s son William Knight was old enough to take it on; James Austen refused to take on a living on this basis as a matter of principle, thereby losing the income he might have received in the meantime.

These restrictions on the sale of an advowson and the potential profits are reflected in the novels. The sale of the right to make the next presentation of the Mansfield living to raise money to pay Tom’s debts must have taken place while Mr. Norris was still alive. One could not buy the right of next presentation and appoint oneself, so Dr. Grant cannot have been the purchaser. The conventional price for the next presentation was five times the annual income of the living, discounted by the likely lifetime of the incumbent. John Dashwood thinks that the Delaford living could have been sold for seven times the amount (£1,400) (SS 334), which may be exaggeration on his part; it is unlikely that the living could have been increased to five times £280, which is £1,400.

The minimum age for ordination as a priest and presentation to a living was twenty-four. Prior to that, the young man would need to be ordained as a deacon, for which the minimum age was twenty-three. These ages were set by ecclesiastical law. The Book of Common Prayer (1662) says: “And none shall be admitted a Deacon, except he be twenty-three years of age. . . . And every man which is to be admitted a Priest shall be full four-and-twenty years old.” This requirement was confirmed by general law in 1804, which seems to have been mainly concerned with its being ignored in Ireland. Austen makes frequent references to the age limit. James Morland must wait between two and three years for the living, “as soon as he should be old enough to take it” (NA 137); Edward Ferrars’s “first boyish attachment to Lucy [is] treated with all the philosophic dignity of twenty-four” (SS 410); Wickham’s story to Elizabeth is that he was excluded from his promised living, which “‘became vacant two years ago, exactly as I was of an age to hold it’” (PP 89); Mr. Collins, at twenty-five, is already a clergyman, so we can assume that he was ordained as a priest the year before and almost immediately visits the Bennets to find a wife. Henry Crawford’s statement that Edmund will have £700 a year from the living at Thornton Lacey “‘[b]y the time he is four or five-and-twenty” (MP 264) seems to add an extra year; however, it may be that Edmund is then about to turn twenty-five and could not have been presented earlier, since his father, the holder of the advowson, was in Antigua and could not sign the necessary documents.

The figures for the value of livings in different novels, because they take place at different dates, are not comparable because of inflation. The following table adjusts the figures to 1813 (when Mansfield Park was published) by taking an average for the previous seven years’ indices for wheat, barley, and oats, which I assume were the crops on which the tithes were based; this formula was later used by Parliament in 1836 for valuing livings when tithes were commuted for a monetary payment (or corn rent). Because prices were rising throughout this period, this calculation provides a very conservative estimate. Following R. W. Chapman, I have taken 1808 as the date of the main action in Mansfield Park, when the value of the Thornton Lacey living is given. I have then taken 1781 as the date of the Norrises’ marriage, a time when their income was very little less than £1,000. Thus if Mrs. Norris brought £7,000, invested at 5% (the average yield of 3% Consols that year was 5.2%), that dowry would produce £350; if their total income was, say, £975, then the Mansfield living was at the time worth £625.

The table demonstrates that stated monetary values of livings (and indeed of anything else) in different novels should not be treated as comparable.

3. The family

A person under twenty-one needed parental consent to marry in England (though not in Scotland, which had its own law). Hence if an English couple eloped to Gretna Green, the nearest place in Scotland, they could be validly married without parental consent. This fact explains why Lydia’s letter to Mrs. Forster indicates that she and Wickham are headed there. No doubt it is where Julia Bertram and Yates go, and where Georgiana Darcy and Wickham would have gone, had they not been prevented from eloping. (The minimum age for marriage in both countries was twelve for girls and fourteen for boys, although marriage so young was most unusual.) In the Austen family, in 1826 Edward Knight’s son Edward eloped to Gretna Green with Mary Dorothea Knatchbull. They were forgiven by Edward Knight, and there was a second marriage in England to keep the elopement out of the newspapers—but the bride’s father, Sir Edward Knatchbull, Edward’s sister Fanny’s husband, never forgave his daughter.

Once a woman was married, her personal property, such as securities, became the property of her husband outright. Although he did not have ownership of her real property (land), he had control of it because she could not dispose of it without his consent. The husband’s rights could be overcome by means of settlements—such as the “‘proper settlement’” made by Mr. Bennet on Lydia of her equal share in the £5,000 to be divided after the deaths of Mr. and Mrs. Bennet (PP 334). That settlement will keep the money out of Wickham’s hands. It was also possible to transfer property to the husband for the separate use of the wife, who could deal with it in equity as if she were unmarried. If a wife survived her husband, the land continued in her ownership, but her former personal property passed under her husband’s will, although she could keep her clothes and the like (paraphernalia). Jointure is the term for the annuity to a widow under a settlement, as in Mrs. Jennings’s “ample jointure” (SS 43), although the statement that it will “descend to her children” is wrong: the jointure ends on her death (although her children will be better off by not having to bear it after her death). The widow was entitled to dower, the income from one-third of the land if no other provision was made for her; hence the term dowager. (One-third was the usual proportion; it varied in different parts of the country.) There are no examples of dower in Austen’s novels.

To turn to the topic of adoption, for Frank Churchill “it was more than being tacitly brought up as his uncle’s heir, it had become so avowed an adoption as to have him assume the name of Churchill on coming of age” (E 15). There was no law on adoption at the time. His uncle must have made a will in Frank’s favor and persuaded Frank to adopt the name of Churchill. It was the same for Austen’s brother Edward when Thomas Knight made him his heir—although Edward did not change his name to Knight until 1812, when he was forty-five.

Dissolving a family was more difficult. Divorce required an Act of Parliament, because there was then no mechanism for the courts to grant a divorce. Mr. Rushworth has “no difficulty in procuring a divorce” (MP 537), because he can well afford the considerable expense of obtaining an Act of Parliament.

4. Money

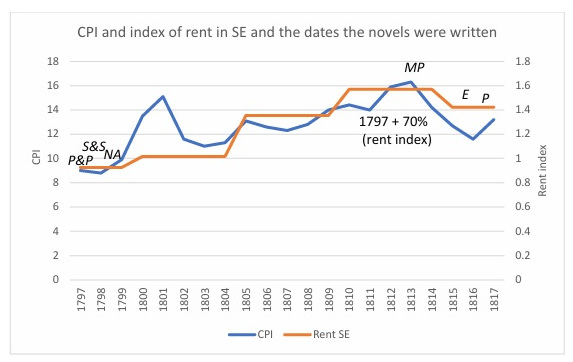

I have already made the point that inflation was a serious matter during Austen’s lifetime. It was a particular problem around 1800; then inflation, according to the Composite Price Index (CPI), was 36.5% in 1800 (the highest figure ever recorded), 11.7% in 1801, and minus 23% in 1802, a drastic change thought to be mainly driven by weather affecting the harvests. The chart below shows two measures of inflation: the CPI (blue); and an index of rents in southeast England (red), using index figures for five-yearly periods, which is less volatile.

The chart shows when the novels were most likely written in relation to these measures of inflation. Using the less volatile rent index, we see that the amount of inflation between Pride and Prejudice and Sense and Sensibility at one end and Emma and Persuasion at the other is 54%. We must treat Mansfield Park separately, as there was a spike in inflation (from 1797 to 1813 it was 70%); Mansfield Park is also a special case because it records events starting thirty years earlier than the main events of the novel.

Since the figures in the early novels were not adjusted before later publication (Avery Jones and Hussain 203), it is therefore important not to compare figures in the 1790s novels with the later ones without adjusting for inflation, or to assume that a figure that indicates a certain standard of living in the earlier novels will apply to the later ones.3 We tend to think in terms of money in the early novels because they contain the most figures; Austen was wise in not including so many in later novels. This change in the value of money is more confusing to us than it would have been to the original readers, who would be aware that matters described related to an earlier period, and they could adjust for this in their minds. I have referred above to the Delaford living of £200 per year; by 1813 the tithes might have amounted to £310. Taking the statement that “‘[t]his little rectory can do no more than make Mr. Ferrars comfortable as a bachelor; it cannot enable him to marry’” (322), by 1813, if one increases the £200 by the CPI, the tithes would need to be increased to £360 to provide the same standard of living.

Directly comparing Mr. Darcy’s income of £10,000 in 1797 pounds with Mr. Rushworth’s £12,000 in 1813 pounds is not meaningful. Using the rent index to adjust for inflation, and assuming that Austen did not revise the numbers for Pride and Prejudice before it was published, we see that Mr. Rushworth’s income in 1797 pounds would be £7,100; Mr. Darcy’s income in 1813 pounds would be £15,400. In other words, Mr. Darcy is much wealthier.

There is a further twist: in 1797, there was no income tax; in 1813, there was a tax of 10%. Thus, since one can spend only income after tax to give the equivalent purchasing power, Mr. Rushworth’s income in 1797 pounds would be £6,400, while Mr. Darcy’s in 1813 pounds would be £17,000. Whichever way we look at it, Mr. Darcy has by far the higher income.

Further, the figure for a person’s income is likely to be the figure before taxes and expenses, so that the person’s income available for spending will be lower. In particular, the landlord of an agricultural tenancy—the typical situation for landed gentry—had high burdens (whether legally required or matters of good estate management) for repairs, land tax, poor rates, tithes, and other liabilities charged on the land, which could easily amount in total to 20% of the gross rent. (I have seen a case where it was 26%.) In Edward Knight’s case, about 12% of his gross rents from his Hampshire properties between 1808 and 1819 were spent on repairs (Slothouber 40). It would not matter if the repairs related to his occupation of Chawton House, since he was taxable on the imputed rent as occupier. Income tax relief for repairs was limited to 8% of the rent in 1799, and reduced to 5% (houses) and 2% (farm buildings) in 1803; the relief was abolished in 1806.

Then there were taxes on luxury items that, at least in theory, were matters of personal choice: carriages, horses, and male servants. These taxes were progressive, so that the tax on 11 male servants (the top band) was 3.2 times the rate per servant as the tax on 1 servant; the tax on 20 horses was 2.2 times the rate per horse as the tax on 1 horse. The window tax was also assessed, although not limited to luxury premises; the rate scale went from 6 or fewer up to 180 windows. To this day, one can see examples of windows blocked up to put the house into the next lower band.

Other than land, the principal investment was in the Funds—undated government securities such as 3% Consols, the quoted price of which varied with interest rates. (Short for “consolidated stock,” Consols derived from a consolidation in 1752 of all existing government stock into a single series of 3½% stock, the rate on which was reduced in 1757 to 3%.) Consols of a nominal value of £100 (at 3%) yielded £3 income per annum forever, but the actual return depended on the cost, which was as low as around £50 per nominal £100 Consols in 1798. In that case, the actual return was around 6% (£3 per annum on the cost of £50). Only a few years earlier, in 1792, the price had been £90, so that the actual return was only 3.3%. Such income was secure but particularly vulnerable to inflation. Mr. Collins refers to Elizabeth’s “‘one thousand pounds in the 4 per cents’” (PP 119), meaning 4% Consols, another large issue of the time. Whether 3% or 4% Consols, the quoted price takes into account the difference in nominal yield. A stock with a higher nominal yield was Navy 5% Annuities (popularly known as Navy Fives), in which Jane Austen invested the proceeds of Pride and Prejudice and Sense and Sensibility in July 1813, buying £300 nominal for about £257, and the proceeds of Mansfield Park in July 1815, buying a further £300 nominal for about £253.

5. Wills

English law does not require any shares to be left by will to specified relatives. A testator can just cut somebody out. The expression “cut someone off with a shilling” strictly refers to trusts, where it was once thought that if one had a power to appoint funds among a class of beneficiaries, one had to give every beneficiary something. With a will, nothing need be paid.4

Land devolved on the heir (who might under the will hold it in trust for someone else), but personal property devolved on the executor, whose role was to give effect to the terms of the will. The executor’s right to deal with the estate was confirmed by the Probate Court, known in the south of England as Doctors’ Commons, by the grant of probate.

Some people have been puzzled by the absence of witnesses to Jane Austen’s own will. At the time no witnesses were required for wills dealing only with personal property, but three witnesses were required for wills dealing with land. The position changed in 1837, when two witnesses were required in all cases. Commonly, if there were no witnesses (and occasionally even if there were), the Court required an independent party’s identification of the handwriting of the will as the testator’s; this was an administrative requirement. The handwriting of Jane Austen’s will was confirmed by an affidavit by John Grove Palmer, the father of Charles Austen’s first wife, Fanny, and Harriet Ebel Palmer, Fanny’s sister, who would later become Charles’s second wife. If there was no will (or if the executor appointed by the will had died), personal property devolved on an administrator appointed by the Probate Court by “letters of administration” in accordance with the intestacy rules (or, if the executor had died, in accordance with the will). The executor or administrator had to swear an oath to administer the estate according to law. Unlike the rest of the common law, until 1857 probate was a matter of ecclesiastical law—in the south of England under the jurisdiction of the Archbishop of Canterbury, and in the north under that of the Archbishop of York. Scotland had its own law, deriving from French civil law.

There were two types of death duties. Probate duty, which effectively still exists, was based on the value of personal property of the estate and was graduated in bands of value. Commonly one sees in the probate documents a marginal note, such as “Under £800,” as was the case with Jane Austen’s probate. This notation indicates that the estate was in the £600–£800 range; sometimes this notation is the only indication of the value of the estate. In Austen’s case, we know that the value was £781 and that the duty was £15.

The second duty was legacy duty, modeled on the Dutch tax that Adam Smith had recommended. This was also restricted to personal property and depended on the relationship between the deceased and the legatee, with close relatives paying a nil or low rate, more remote relatives paying an increasingly higher rate, and unrelated people paying the top rate (10% at the time of Jane Austen’s death). This difference in rates sounds reasonable, but it had the strange effect that small legacies to servants were liable for the top rate. In Jane Austen’s case she left two legacies, both of £50—one to her brother Henry, who paid 3% duty, and the other to his former servant Madame Bigeon, who was responsible for 10%. Another occasion where this duty gave strange results can be seen in the estates of Mr. and Mrs. Leigh Perrot. He left his estate to his wife, partly outright and partly for life. On her death she left about half of her estate to James Austen’s son, James Edward Austen (with the stipulation that he take the name Austen-Leigh); he was responsible for the top rate of 10%, because he was related to her only through marriage. The remainder interest under her life interest of the legacy by Mr. Leigh Perrot to James was 3%. The records of the Legacy Duty Office, all of which have survived in England, are particularly useful in showing this type of financial information about estates.5

Connected with wills are deathbed promises such as John Dashwood’s promise to “do every thing in his power to make [his sisters and stepmother] comfortable” (SS 5). Since Henry Dashwood on his deathbed promised nothing in return, there was no contract, and John’s promise was unenforceable in law (and in any case was probably too vague to be enforced anyway). The law would enforce the promise even though it was not in the will; it would then be a secret trust—secret because it was not set out in the will but still enforceable as a trust, which did not need to be in writing.

In addition, people commonly left letters of wishes that were not enforceable in law, leaving chattels to various beneficiaries to avoid setting them out in the will and to enable them to be changed afterwards without changing the will itself. Jane Austen’s estate provides a good example. Cassandra, demonstrating that she knew that such wishes were not legally enforceable, wrote to Fanny Knight after Jane’s death: “I have found some Memorandums, amongst which [Jane] desires that one of her gold chains may be given to her God-daughter Louisa & a lock of her hair be set for you. You can need no assurance my dearest Fanny that every request of your beloved Aunt will be sacred with me. Be so good as to say whether you prefer a broche or ring” (29 July 1817).

![]()

I began by saying that Austen assumed of her readers a certain knowledge of English culture and law of the time. I hope that this essay has served to fill in any gaps in the knowledge of her global readers.

NOTES

1Legal aspects are authoritatively dealt with by G. H. Treitel (Vinerian Professor of English Law at Oxford University). I have drawn on these articles for many points in this article.

2It is interesting that the first edition says “by any division of the estate”; someone, probably her brother Henry, must have put Austen right about this.

3I have made, but not yet published, a similar analysis of the figures in Pride and Prejudice, reaching the same conclusion.

4Copies of wills probated in England before 1858 by the Prerogative Court of Canterbury are available for download from the English National Archives in the series PROB 11. For more information, see https://www.nationalarchives.gov.uk/help-with-your-research/research-guides/wills-or-administrations-before-1858/. There is a separate series, PROB 1, containing wills of famous people, including Jane Austen’s. Original wills not available for download are also in the National Archives, indexed according to the month and year probate was granted and the initial letter of the surname.

5To find such records, go to http://www.findmypast.co.uk (free within the National Archives and some libraries, or subscribe) and search for the folio number; then go to https://www.familysearch.org/en/; then Search/catalog/keywords and enter “death duty”; then choose, e.g., https://www.familysearch.org/search/catalog/614554 Death duty register for wills in the Prerogative Court of Canterbury and country courts, 1812-1857.